Labour Market

The labour market continues to improve due to central bank support, with unemployment having fallen to a historical low of 6.8 percent in February. A clear signal of robust demand for labour emerge, but still long way to go due to muted wage growth. It is expected with reopen of the economy to full capacity should support faster growth in wages.

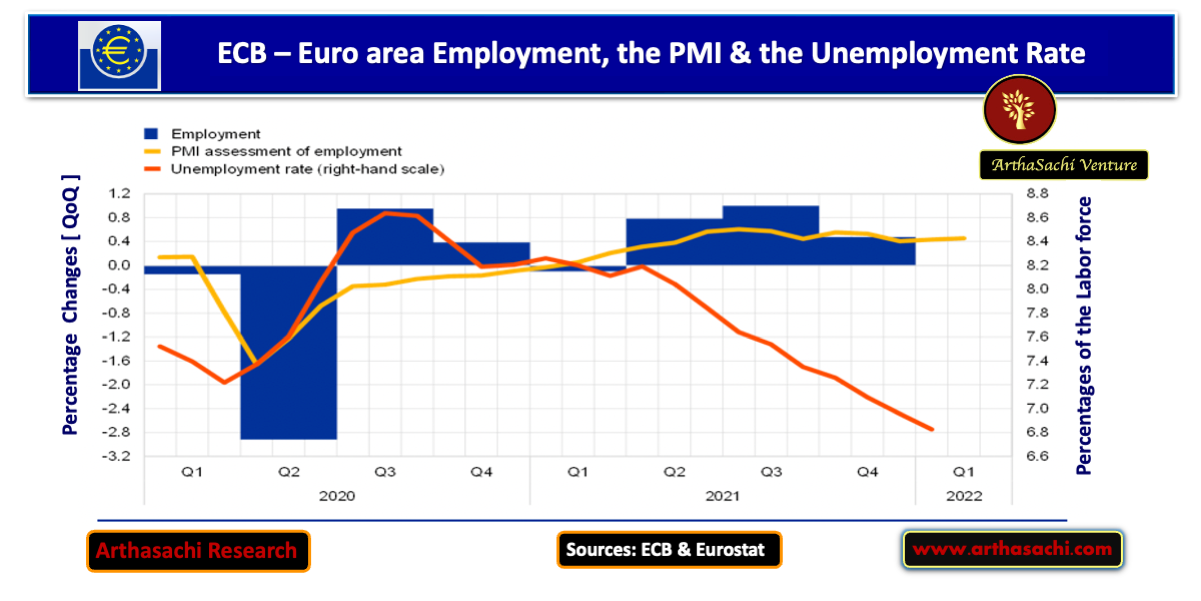

The euro area labour market strengthened further in the fourth quarter of 2021.

Employment grew by 0.5%, quarter on quarter, in the fourth quarter of 2021, surpassing its pre-pandemic level. Strengthening labour demand was also reflected in a further increase in the aggregate job vacancy rate, which rose to a new series high of 2.7% in the fourth quarter of 2021. Moreover, this rise was more broad-based across sectors. The size of the labour force and the labour force participation rate returned to close to their pre-pandemic levels in the fourth and third quarters of 2021 respectively. After averaging 7.1% in the final quarter of 2021, the unemployment rate declined further to stand at 6.8% in January 2022. However, support from job retention schemes remained substantial, with their use ticking up slightly to 1.5% of the labour force in January as containment measures were reimposed.

The monthly composite Purchasing Managers’ Index (PMI) employment indicator, which encompasses both industry and services, stood at 54.5 in February, broadly unchanged from January and well above the threshold of 50 that indicates growth in employment. This outcome was recorded despite an intensification of the pandemic during the first few weeks of the year and reported difficulties in filling vacancies. By contrast, some downward pressure on average hours worked was likely due to absences related to the Omicron variant, although this was possibly attenuated by co-workers increasing their hours.

Apps

Dowload Our "Arthasachi Venture Wealth" Apps

Apple IOS App

Andriod App