Bond Markets started the year with a record Interest from the Investor

Bond Markets fuel an unprecedented interest from the Investor for the governments and corporates bonds around the world; funded close to half a trillion dollars through debt instruments in January 2023 till now.

The Fed has been increasing interest rate at a pace never seen in decades as it struggling to bring down inflation, announced seven rates hiked in 2022. The Fed with December hike of 50 Basis points moved the key short-term rate to a range of 4.25% to 4.5%, its highest level in 15 years. Dollar weakness continued with successive rate hike. The era of Dollar strength is over and dusted now; dollar index inching closer to 7-month low. Fed still expects rates to rise higher than previously forecast, senior officials are unsure just how much further they will raise rate. The Fed’s economic staff said a recession was possible in the next year. US CPI December rose to 6.5% YoY down from 7.1% in the Nov 22. In Sep it was highest since 1982 which hit 40 Year High.

The Fed chair, Jerome Powell, has indicated that rate rises may slow down as inflation declines, but he maintained that rates will remain high until inflation is brought down to the central bank’s target rate of 2%. The US jobs market which recorded its second strongest year of growth on record 2022 added Fed worries; overheated labor market could add to inflationary pressure. The latest CPI report is unlikely to quell those concerns. Downward movement of December CPI number has resulted in the US Bond Market showing sign of softening of interest rate since last few weeks. All eyes are on 31st Jan FOMC meetings. US Treasury’s 10 Year Bond yield dropped 2 Basis Points this week and 39 Basis Points drop in Jan 2023 and closed at 3.48%.

Bank of England hikes another 50 Basis points Interest Rates, largest successive hike since 1989 on 15th DEC 22 meeting its seventh times since December 2021, to lift its key rate to 3.5%. Its biggest rate increases in 27 years despite growing risks of a prolong recession. As per Bank of England forecasts, Britain has already entered a recession that could potentially last till 2024. GDP is projected to continue to fall through out 2023 and 2024 H1 warned of a “very challenging outlook.” The Committee stated, “There are considerable uncertainties around the outlook.” Andrew Bailey, the Bank’s Governor, defended the sharp rise in Interest rates, commented “If we do not act forcefully now, it will be worse later on.” It’s a tough road ahead he added. Inflation hits 41 Year high of 11.1% in Oct 22 which dropped to 10.7% in NOV 22. UK is fighting a higher Inflation; annual inflation rate jumped to 11.1% in October 2022 with the target to keep it at 2%. It is the highest inflation rate since October 1981. The British economy shrank 0.2% on quarter in Q3 2022, the first contraction in 1-1/2-years. Earlier Moody’s downgraded UK, cut the outlook to “Negative” from “Stable”. UK Treasury’s 10 Year Bond closed at 3.37% with a weekly loss of 1 Basis Points and it lost 30 Basis Points in January 2023 alone.

European Central Bank raised Interest Rates by 50 Basis Points and expect to raise them significantly higher. As per December 2022 ECB projections for Euro area economic growth in 2022 will be 3.4% and the coming years; 2023 0.5% ; 2024 1.9% and for 2024 expected to be 1.8%. Economic growth in the Euro area slowed to 0.3% in the Q3 of 2022. Risks to the economic growth outlook are on the downside, especially in the near term. ECB CPI Inflation moderated to 10.0% in November 2022. Inflation projection 2022 8.4%; 2023 6.3% and for 2024 3.4%. Inflation is far too high and will remain high for too long well above 2% target, the EU economy is going through a difficult time. ECB in March will start to reduce the large amount of bonds they bought over the past few years as part of their asset purchase programme. German inflation (HICP) after hitting all time high fell to 10.0 percent in November month down from October’s all time high of 10.4%. Germany Treasury’s 10 Year Bond has seen 1 Basis points drop this week, lost 39 Basis Points in January 2023 alone and closed at 2.17%.

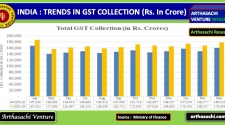

India’s GDP is estimated to grow by 7% in 2022-23 as per Indian Government. In the Financial year 2021-22 GDP has grown by 8.7%. RBI has raised the Repo Rate by 35 BPS taking the headline rate to 6.25% in its Monetary Policy meeting on 7th DEC 2022. India’s headline inflation (CPI) rate fell to 5.71% in December 2022, eased to one year low. Inflation is below repo rate which is currently at 6.25% which reflect how well RBI managed the growth and inflation vis-à-vis its counterpart Federal Reserve, ECB, Bank of England etc. Monetary policy in India started yielding results. The Inflation fell below RBI target rate of 2-6% for the first time this year. India Treasury’s 10 Year Bond has seen 6 Basis Point gain this week and closed at 7.35%. We expect such measures will help to retain the growth momentum and to push the Indian economy to a high growth trajectory in the next 2-3 years period.

Top News

Other News

MARKETS

WEALTH

ECONOMICS

START UP

TECHNOLOGY

BUSINESS

Alliances and Partners

Arthasachi Venture Footprints

Apps

Dowload Our "Arthasachi Venture Wealth" Apps

Apple IOS App

Andriod App