State Bank of India Reports Robust Q3FY25 registered a Net Profit growth of 84% on YoY

Mumbai, February 6th, 2025 – State Bank of India (SBI), the country’s largest public sector bank with a branch network of 22.74 thousand, announced its financial results for the third quarter (Q3FY25) and the nine-month period ending December 31, 2024.

The results reflect strong growth in profitability, improved asset quality, and sustained credit growth across key segments. SBI’s performance underscores its resilience and ability to navigate a challenging economic environment while maintaining robust operational efficiency.

Key Highlights of Q3FY25 and Nine-Month FY25 Performance

Profitability

- Net Profit: SBI reported a net profit of ₹16,891 crores for Q3FY25, marking an impressive 84.32% year-on-year (YoY) growth compared to ₹9,164 crores in Q3FY24. However, on a quarter-on-quarter (QoQ) basis, net profit declined by 7.86% from ₹18,331 crores in Q2FY25.

- Operating Profit: Operating profit for Q3FY25 grew by 15.81% YoY to ₹23,551 crores, though it declined by 19.60% QoQ from ₹29,294 crores in Q2FY25.

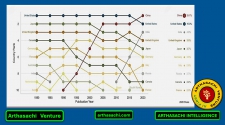

- Return on Assets (ROA): ROA has improved from 0.02% for FY19 to 1.04% for Q3FY25 indicating strong returns for the shareholders, also an improvement of 42 basis points (bps) YoY. For the nine-month period (9MFY25), ROA was 1.09%, reflecting the bank’s efficient asset utilization.

- Return on Equity (ROE): ROE has improved from 0.48% in FY19 to 21.46% for 9MFY25, indicating strong returns for shareholders.

Net Interest Income (NII) and Margins

- Net Interest Income (NII): NII for Q3FY25 increased by 4.09% YoY to ₹41,446 crores. However, it saw a marginal decline of 0.42% QoQ from ₹41,620 crores in Q2FY25.

- Net Interest Margin (NIM): Domestic NIM for Q3FY25 stood at 3.15%, down by 19 bps YoY and 12 bps QoQ. For 9MFY25, domestic NIM was 3.25%, reflecting a decline of 16 bps YoY.

Balance Sheet Growth

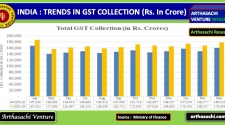

- Gross Advances: SBI’s gross advances crossed the ₹40 lakh crore mark, growing by 13.49% YoY to ₹40,67,752 crores. On a QoQ basis, advances grew by 3.75%.

-

- Domestic Advances Grew by 14.06% YoY, with Corporate Advances up by 14.86% YoY, Retail Personal Advances up by 11.65% YoY, and Home Loans growing by 14.26% YoY. SME Advances Grew by 18.71% YoY, while Agriculture Advances increased by 15.31% YoY.

- Deposits: Whole bank deposits grew by 9.81% YoY to ₹52,29,384 crores.

- CASA Deposits grew by 4.46% YoY, though the CASA ratio declined to 39.20% from 41.18% in Q3FY24. Liability franchise accounts of over 22% of domestic market share.

Asset Quality

- Gross NPA Ratio: Improved by 35 bps YoY to 2.07% in Q3FY25, though it saw a marginal increase of 6 bps QoQ.

- Net NPA Ratio: Improved by 11 bps YoY to 0.53%, remaining stable on a QoQ basis.

- Provision Coverage Ratio (PCR): PCR (including AUCA) improved by 25 bps YoY to 91.74%, while PCR (excluding AUCA) improved by 49 bps YoY to 74.66%.

- Slippage Ratio: Improved by 19 bps YoY to 0.39% in Q3FY25, reflecting better asset quality management.

- Credit Cost: Stood at 0.24% for Q3FY25, up by 3 bps YoY but down by 14 bps QoQ.

Capital Adequacy

- Capital Adequacy Ratio (CAR): SBI’s CAR stood at 13.03% as of Q3FY25, slightly lower than 13.76% in Q2FY25 well above with regulatory requirements.

Alternate Channels

- Digital Banking: SBI continues to leverage its digital platform, YONO, with 64% of savings bank accounts acquired digitally through YONO in Q3FY25, 8.45 crore registered customers. The share of alternate channels in total transactions increased from 97.7% in 9MFY24 to 98.1% in 9MFY25, reflecting the bank’s focus on digital transformation.

Key Financial Metrics (Q3FY25 vs. Q3FY24 and Q2FY25)

|

Metric |

Q3FY24 |

Q2FY25 |

Q3FY25 |

YoY Growth |

QoQ Growth |

|

Net Profit |

₹9,164 cr |

₹18,331 cr |

₹16,891 cr |

84.32% |

-7.86% |

|

Operating Profit |

₹20,336 cr |

₹29,294 cr |

₹23,551 cr |

15.81% |

-19.60% |

|

Net Interest Income |

₹39,816 cr |

₹41,620 cr |

₹41,446 cr |

4.09% |

-0.42% |

|

Gross Advances |

₹35,84,252 cr |

₹39,20,719 cr |

₹40,67,752 cr |

13.49% |

3.75% |

|

Deposits |

₹47,62,221 cr |

₹51,17,285 cr |

₹52,29,384 cr |

9.81% |

2.19% |

|

Gross NPA Ratio |

2.42% |

2.13% |

2.07% |

-35 bps |

-6 bps |

|

Net NPA Ratio |

0.64% |

0.53% |

0.53% |

-11 bps |

0 bps |

Analysis of YoY and QoQ Performance

Year-on-Year (YoY) Analysis

- Profitability: SBI’s net profit surged by 84.32% YoY, driven by higher interest income and improved asset quality. Operating profit also grew by 15.81% YoY, reflecting strong core banking operations.

- Credit Growth: Whole Bank advances crossed ₹40 trillion grew by 13.49% YoY, with foreign office’s advances grew by 10.35%, SME and Agri advances grew by 18.71% and 15.21%; while Corporate and Retail Personal advances registered 14.86% and 11.65% respectively demonstrate growth across the sectors.

- Deposit Growth: Whole Bank Deposits cross ₹52 trillion grew by 9.81% YoY, though CASA ratio stands at 39.20% as on 31st Dec 24 growth was slower at 4.46% YoY.

- Asset Quality: Gross NPA and Net NPA ratios improved by 35 bps and 11 bps YoY at 2.07% and 0.53% respectively, indicating better credit risk management.

Quarter-on-Quarter (QoQ) Analysis

- Profitability: Net profit declined by 7.86% QoQ, primarily due to higher loan loss provisions and a slight decline in NII. Operating profit also fell by 19.60% QoQ, reflecting seasonal fluctuations.

- Credit Growth: Advances grew by 3.75% QoQ, with retail and corporate segments driving the growth.

- Deposit Growth: Deposits increased by 2.19% QoQ, though CASA deposits saw a marginal decline.

- Asset Quality: Gross NPA ratio increased by 6 bps QoQ, while Net NPA ratio remained stable. Slippage ratio improved by 19 bps QoQ, indicating better recovery efforts.

Conclusion

SBI’s Q3FY25 results demonstrate its ability to deliver strong financial performance despite macroeconomic challenges. The bank’s focus on digital transformation with over 98% transactions through alternate channels, coupled with robust credit growth well above Industry average and improved asset quality, positions to Lead the Indian Banking to the next level of growth. While there are some pressures on margins and profitability on a QoQ basis due to prudent approach, the YoY growth highlights SBI’s resilience and operational strength.

About State Bank of India (SBI)

State Bank of India is the largest public sector bank in India, with a vast network of branches and a strong presence in both domestic and international markets. The bank offers a wide range of financial products and services, catering to the diverse needs of its customers. SBI continues to lead the way in digital banking innovation, with its YONO platform being a key driver of customer acquisition and engagement.

Top News

Other News

MARKETS

WEALTH

ECONOMICS

START UP

TECHNOLOGY

BUSINESS

Alliances and Partners

Arthasachi Venture Footprints

Apps

Dowload Our "Arthasachi Venture Wealth" Apps

Apple IOS App

Andriod App